The evolution of on-chain derivatives markets has pushed decentralized trading platforms beyond simple token swaps. With rising demand for options, perpetual futures, and leveraged trading, on-chain protocols are increasingly adopting traditional financial infrastructure like order books, risk engines, and margin systems.

Within the on-chain derivatives arena, Derive positions itself as a professional-grade trading platform. Its core mission is to deliver a trading experience comparable to centralized exchanges—all within a self-custody environment. To achieve this, Derive integrates a Layer2 network, a Central Limit Order Book (CLOB), Portfolio Margin, and on-chain settlement to build a complete trading infrastructure covering order matching, risk assessment, and capital management.

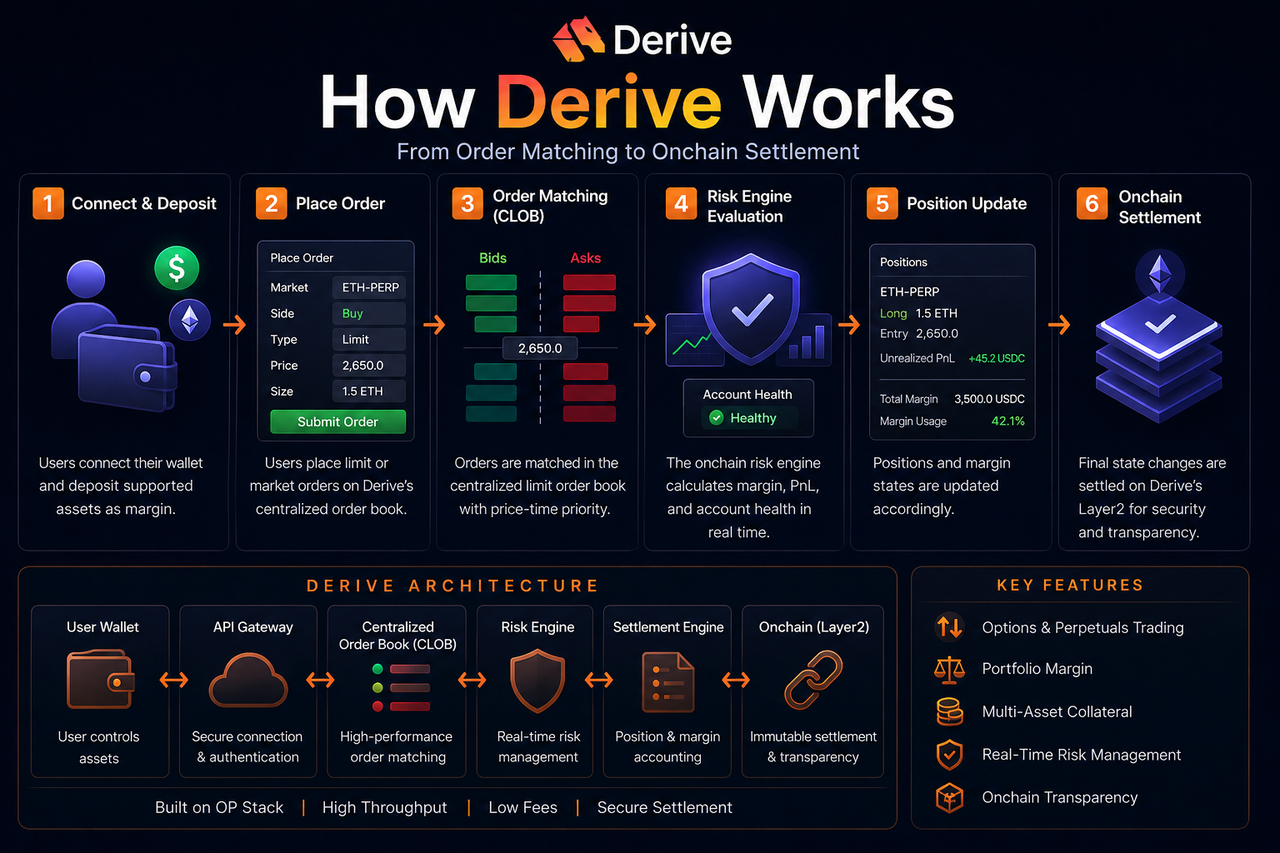

What Makes Up Derive's Trading System?

Derive's trading system comprises an order book, risk engine, margin system, settlement module, and Layer2 network. These components work together to form a complete on-chain derivatives trading pipeline.

The order book handles order placement and matching, the risk engine continuously evaluates account risk and margin requirements, and the settlement system manages position updates, asset transfers, and on-chain state synchronization.

Unlike traditional AMM models, Derive favors an order-driven market structure. The order book model is naturally suited to derivatives trading, enabling more sophisticated pricing and more efficient liquidity management.

Derive's underlying network is built on the OP Stack, allowing the protocol to achieve lower Gas costs and higher transaction throughput within a Layer2 environment.

How Do Users Start Trading on Derive?

Before trading, users must create an account and deposit collateral.

As a self-custody protocol, Derive lets users retain control of their assets through their on-chain wallets. Users typically deposit stablecoins or other supported collateral into the protocol, which becomes their margin account balance.

Derive supports multi-asset collateral, meaning users aren't restricted to a single stablecoin as margin. The system calculates collateral value and risk exposure based on each asset's risk parameters.

Once margin is deposited, users can trade options or perpetual futures on the order book. Available margin adjusts dynamically as positions change.

How Are Orders Matched on Derive?

Derive uses a Central Limit Order Book (CLOB) for order matching.

Users can submit limit or market orders. Orders enter the book and are matched on a price-time priority basis. When buy and sell prices match, the order executes and both parties' positions are updated.

The order book model offers more precise price discovery than AMMs—especially critical in options markets where varying strike prices, expiration dates, and volatility create complex pricing structures. This makes the order book ideal for professional derivatives trading.

While Derive relies on a high-performance matching engine, all final position states and capital changes sync to the on-chain network, ensuring transparency and verifiability.

How Does Derive's Risk Engine Evaluate Account Risk?

The risk engine is one of Derive's most critical modules.

Since users may hold multiple perpetual and options positions simultaneously, the system can't assess risk in isolation. Derive uses Portfolio Margin to evaluate the entire account's net risk exposure.

For example, if a user holds both long and short positions, some risks offset, allowing the system to reduce the overall margin requirement. This boosts capital efficiency compared to isolated margin models.

The risk engine monitors multiple metrics in real time:

| Risk Indicator |

Function |

| Account Equity |

Measures overall asset status |

| Initial Margin |

Minimum margin to open a position |

| Maintenance Margin |

Minimum balance to avoid liquidation |

| Volatility Parameters |

Adjusts risk weights for different assets |

| Liquidity Depth |

Assesses market impact risk |

The system dynamically adjusts risk parameters based on market volatility to reduce systemic risk during extreme events.

When Does Derive's Liquidation Mechanism Trigger?

Liquidation is triggered when an account's margin falls below the maintenance margin requirement.

The liquidation system is designed to prevent accounts from going insolvent. If rapid price moves widen losses, the system automatically reduces or closes positions to restore the account to a safe level.

Under the Portfolio Margin model, the system evaluates overall account risk first—it doesn't liquidate positions in isolation. This means hedged positions can help lower the chance of liquidation.

However, in highly volatile, low-liquidity markets, slippage and liquidation losses may increase. Risk management remains a critical part of on-chain derivatives trading.

How Does the Perpetual Futures Funding Rate Work?

Perpetual futures have no expiration, so a funding rate mechanism keeps the contract price aligned with the spot market.

When the perpetual price is above the spot price, longs typically pay the funding rate to shorts, and vice versa.

This mechanism incentivizes traders to adjust their positions, reducing price divergence.

On Derive, the funding rate dynamically adjusts based on market supply, demand, and position structure. High leverage and extreme conditions often cause the funding rate to spike.

How Does Derive Differ from Traditional Centralized Exchanges in Trading Process?

The key differences lie in asset custody and settlement.

On centralized exchanges, users deposit assets into platform-controlled accounts. On Derive, users keep control via their on-chain wallets, while the protocol handles trading and risk management.

Centralized exchanges use fully offline matching and database updates, whereas Derive must sync final trade states to the chain, requiring a balance between performance and decentralization.

Through its Layer2 and high-performance order book architecture, Derive has already narrowed the experience gap with centralized exchanges significantly.

Derive's Advantages and Potential Limitations

Derive's core strengths are high capital efficiency and professional-grade trading. Portfolio Margin, multi-asset collateral, and the order book model enable complex strategies.

The Layer2 network reduces transaction costs and boosts order processing speed—critical for high-frequency derivatives.

However, the architecture brings greater complexity. Options, margin, and risk management can be challenging for everyday users.

Additionally, on-chain protocols face smart contract, cross-chain, and liquidity risks. Insufficient market depth can degrade the order book experience.

Conclusion

Derive is a professional trading protocol for on-chain derivatives, covering order matching, margin management, risk assessment, liquidation, and on-chain settlement. By leveraging a Layer2 network, Central Limit Order Book, and Portfolio Margin, Derive aims to deliver a trading experience in a self-custody environment that rivals traditional professional exchanges.

FAQs

What is Derive's Portfolio Margin?

Portfolio Margin assesses the entire account's risk exposure rather than calculating margin for each position individually.

Why does Derive need a Layer2 network?

Layer2 reduces Gas costs and increases transaction speed, making it ideal for high-frequency derivatives trading.

How does Derive's liquidation mechanism work?

When account margin falls below the maintenance margin requirement, the system automatically reduces or closes positions to mitigate overall risk.

What does the perpetual futures funding rate do?

It keeps the perpetual futures price aligned with the spot price.

What's the difference between Derive and centralized exchanges?

Derive prioritizes self-custody and on-chain settlement transparency, while centralized exchanges typically use a platform custody model.