Real World Asset Tokenization (RWA) is rapidly becoming one of the most important trends in the blockchain industry. Having proven the viability of fiat currency digitization through stablecoins, traditional financial assets such as stocks, ETFs, and bonds are now progressively moving on-chain. A growing number of institutions aim to leverage blockchain technology to boost asset circulation efficiency, shorten settlement times, and widen access for global investors — and tokenized stocks are a key piece of this transformation.

In the U.S. market for tokenized securities, Dinari stands out as one of the most closely watched infrastructure projects in recent years. As a fintech company specializing in Tokenized Stocks, Dinari seeks to bring U.S. capital market equities onto blockchain networks through a compliant issuance framework and on-chain infrastructure.

What Is Dinari

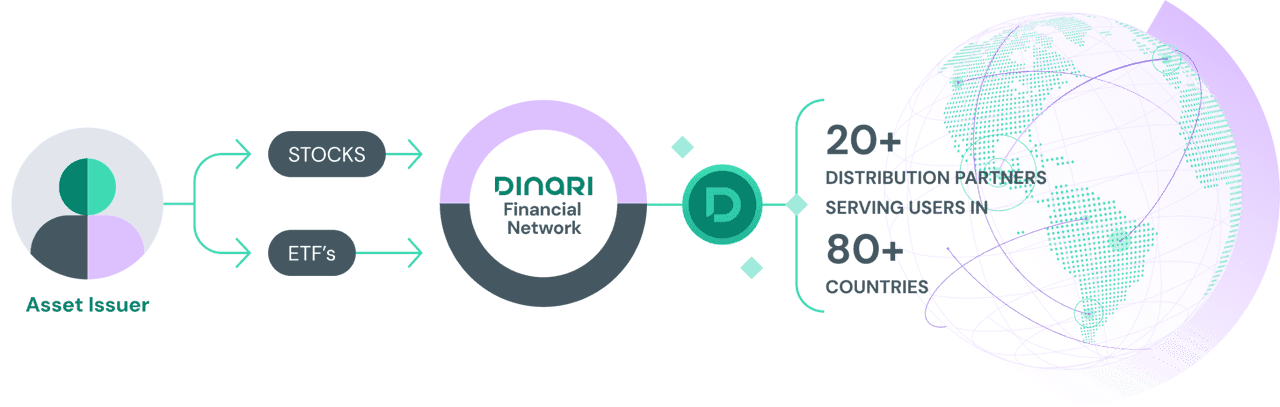

Dinari is a U.S.-based fintech company focused on issuing tokenized securities and building the underlying infrastructure. Its core mission is to map U.S. stock market assets into digital assets on blockchain networks. Through real stock custody, carefully designed legal structures, and on-chain issuance mechanisms, Dinari gives traditional securities a digital form that can be circulated and managed within the blockchain ecosystem.

Unlike many on-chain assets that merely track price movements, Dinari places strong emphasis on real asset backing and regulatory compliance. Its goal is not to create a new stock exchange but to build a digital mapping layer atop the existing securities system, allowing stock assets to seamlessly integrate into the evolving digital financial ecosystem.

What Are Dinari’s dShares?

dShares is Dinari’s core tokenized stock product line and the most important component of its infrastructure. Each dShare typically represents a specific amount of an underlying real stock, with asset backing maintained through custodians and legal arrangements. This allows stock assets to be converted into digital tokens that can circulate on blockchain networks.

From a user perspective, dShares behave much like any other digital asset — they can be stored in digital wallets and transferred on-chain. However, their value fundamentally derives from the corresponding real stocks, making them a significant practical application of real-world asset tokenization.

How Dinari Tokenizes Stocks

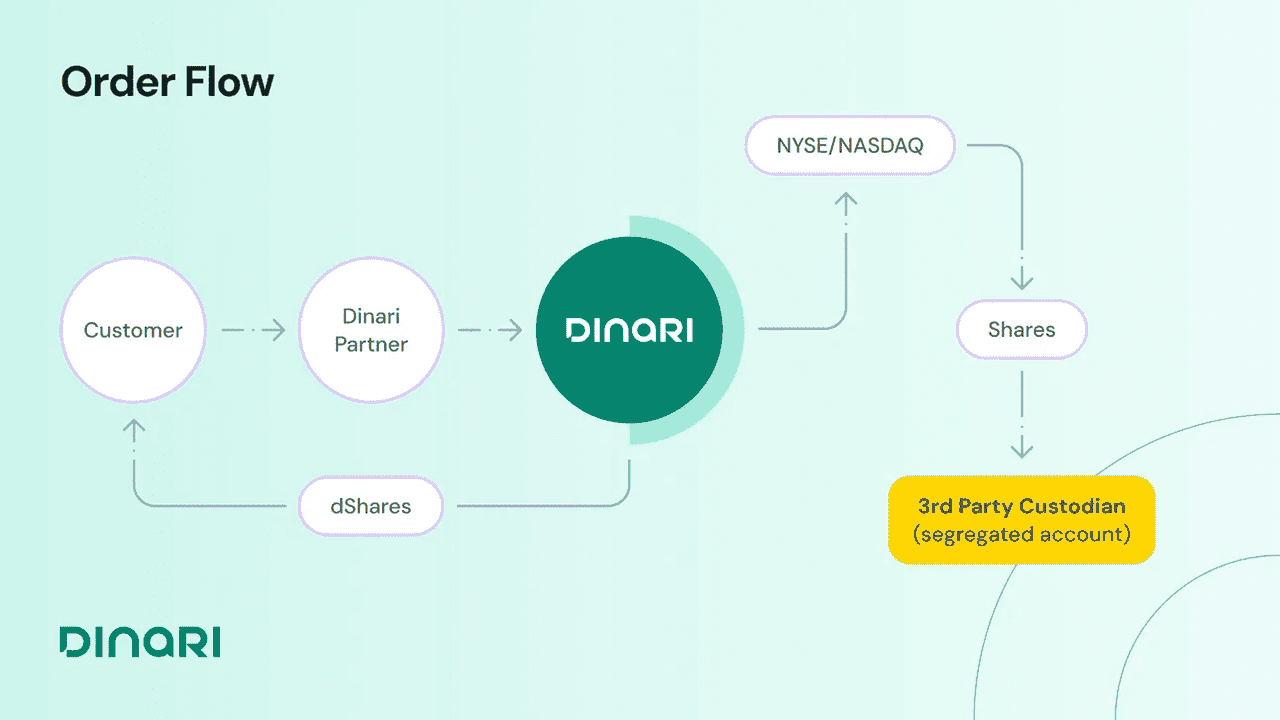

Dinari’s tokenization process is built on real securities backing. First, the issuance system purchases the corresponding stocks through compliant channels, with a professional custodian holding the assets. A legal entity then establishes a clear mapping between on-chain tokens and the underlying securities to define asset ownership and investor rights.

Once asset custody and legal structures are in place, the system issues a corresponding number of dShares based on actual holdings. The entire process does not alter the equity structure of the listed company, but instead creates a digital on-chain mapping layer on top of existing stocks. This enables traditional stocks to enter the blockchain ecosystem and gain new circulation use cases.

What Makes Dinari’s Compliance Architecture Unique?

Compliance is one of Dinari’s strongest competitive advantages and a key differentiator from many early on-chain securities projects. Since stocks are heavily regulated financial assets, tokenization involves not just technical challenges but also compliance with securities laws, asset custody rules, and investor protection requirements.

From the outset, Dinari designed its operations around the U.S. regulatory framework, aiming to advance stock digitization while ensuring asset authenticity and investor rights. Real asset custody, identity verification mechanisms, legal structure design, and transparent disclosure practices form the pillars of its compliance architecture — and are major reasons for its market attention.

How Is Dinari Different From Traditional Brokers?

Both Dinari and traditional brokers help investors gain exposure to the stock market, but they rely on completely different infrastructure. Traditional brokers record holdings in securities accounts and depend on exchanges, clearinghouses, and custodian banks for trading and settlement. While investors hold economic rights, they typically cannot directly control the underlying securities records.

Dinari, by contrast, maps stocks into on-chain digital assets via dShares, allowing users to manage their positions through a digital wallet. Asset transfers and settlement occur on the blockchain, giving the process a much stronger digital character. In essence, traditional brokers operate on an account-based system, while Dinari is closer to a blockchain asset-based system — representing two different directions for financial infrastructure evolution.

How Is Dinari Different From Backed Finance?

Dinari and Backed Finance are both major players in the real-world asset tokenization space, but their development paths differ. Backed Finance originated in Europe, focusing on securities tokenization under the European regulatory environment, and has launched multiple tokenized products based on stocks and ETFs.

Dinari, in contrast, focuses more narrowly on the U.S. securities market, building a standardized stock token system around dShares. Both aim to bring traditional securities onto blockchain networks, but they differ in regulatory environment, target market, and product structure design.

What Is the Relationship Between Dinari and xStocks?

Dinari and xStocks are often mentioned together in discussions about tokenized stock markets, but they are not the same project. Dinari is closer to an asset issuer and infrastructure provider, focusing on mapping real stocks to on-chain tokens and building the compliance framework.

xStocks places more emphasis on creating a standardized on-chain stock ecosystem and a unified issuance network, aiming to provide common standards for a wide range of tokenized stock projects. From an industry perspective, they are different participants in the same track, collectively driving the development of the Tokenized Stocks market.

What Challenges Does Dinari Face?

Despite the promising outlook for tokenized stocks, Dinari and its industry face multiple challenges. The regulatory environment remains one of the biggest unknowns, with varying requirements across jurisdictions affecting cross-border distribution and market expansion.

Additionally, on-chain securities markets still have far lower overall liquidity than traditional stock exchanges. Attracting more institutional investors, market makers, and developers to participate in the ecosystem will be critical for growth. Security of asset custody, cross-chain compatibility, and user education are also ongoing challenges that will shape the industry’s evolution.

Dinari Core Features Overview

| Dimension |

Dinari |

| Project Positioning |

U.S. Tokenized Stock Infrastructure |

| Core Product |

dShares |

| Underlying Assets |

U.S.-Listed Stocks |

| Asset Backing |

Real Stock Custody |

| Key Direction |

Compliant Securities Tokenization |

| Track |

RWA, Tokenized Stocks |

| Main Value |

Bridging U.S. Capital Markets and Blockchain Ecosystem |

Summary

As a key infrastructure project in the U.S. real-world asset tokenization space, Dinari maps real stocks into on-chain digital assets through its dShares product line. Its core strengths lie in real asset backing, a regulatory compliance framework, and blockchain-native circulation capabilities, enabling traditional stocks to enter the on-chain financial ecosystem as digital assets.

As the Tokenized Stocks and RWA markets continue to grow, Dinari is exploring a new path for the digitalization of the U.S. securities market. By connecting traditional capital markets with blockchain infrastructure, Dinari not only advances stock asset tokenization but also provides an important reference for the broader onboarding of real-world assets onto the chain.

FAQs

What Are dShares?

dShares is Dinari’s tokenized stock product system, designed to create a mapping relationship between on-chain digital assets and real stocks.

Is Dinari an RWA Project?

Yes. Dinari’s core business involves tokenizing real-world stock assets, making it a key part of the Real World Assets (RWA) track.

What Is the Difference Between Dinari and Traditional Brokers?

Traditional brokers rely on securities accounts and exchange infrastructure, while Dinari issues tokenized stocks through blockchain networks, allowing assets to be held and transferred in digital form.

Which Is Larger: Dinari or Backed Finance?

Both are significant projects in the tokenized securities space, but they target different markets and regulatory environments, making direct comparison difficult.