edgeX - Perp DEX ที่ถูกฟักตัวโดย Amber Group ผู้ทำตลาด Crypto ชื่อดัง

Perp DEX รุ่นนี้มีความแตกต่างอย่างมีนัยสำคัญจาก Perp DEX รุ่น “GMX, DYDX” แม้ว่าหลักยังคงเป็น Perp DEX ดังนั้นหัวข้อยังคงใช้ Perp DEX ในการอภิปราย

บทความนี้เป็นตอนสุดท้ายของซีรีส์ Perp DEX ที่ใช้เวลาหนึ่งเดือน โดยเน้นไปที่สมาชิกคนสุดท้ายใน Perp DEX F4 (อันดับสี่แรกใน DefiLlama) —— edgeX และขยายไปสู่การพูดคุยถึงสถานการณ์และแนวโน้มของตลาด Perp DEX ทั้งหมด

เมื่อผู้เล่นหลักในตลาดเริ่มลงตัวแล้ว ช่วงฮอตของ Perp DEX อาจจะจบลง ผู้เล่นใหม่จะเข้ามายากขึ้นเรื่อย ๆ

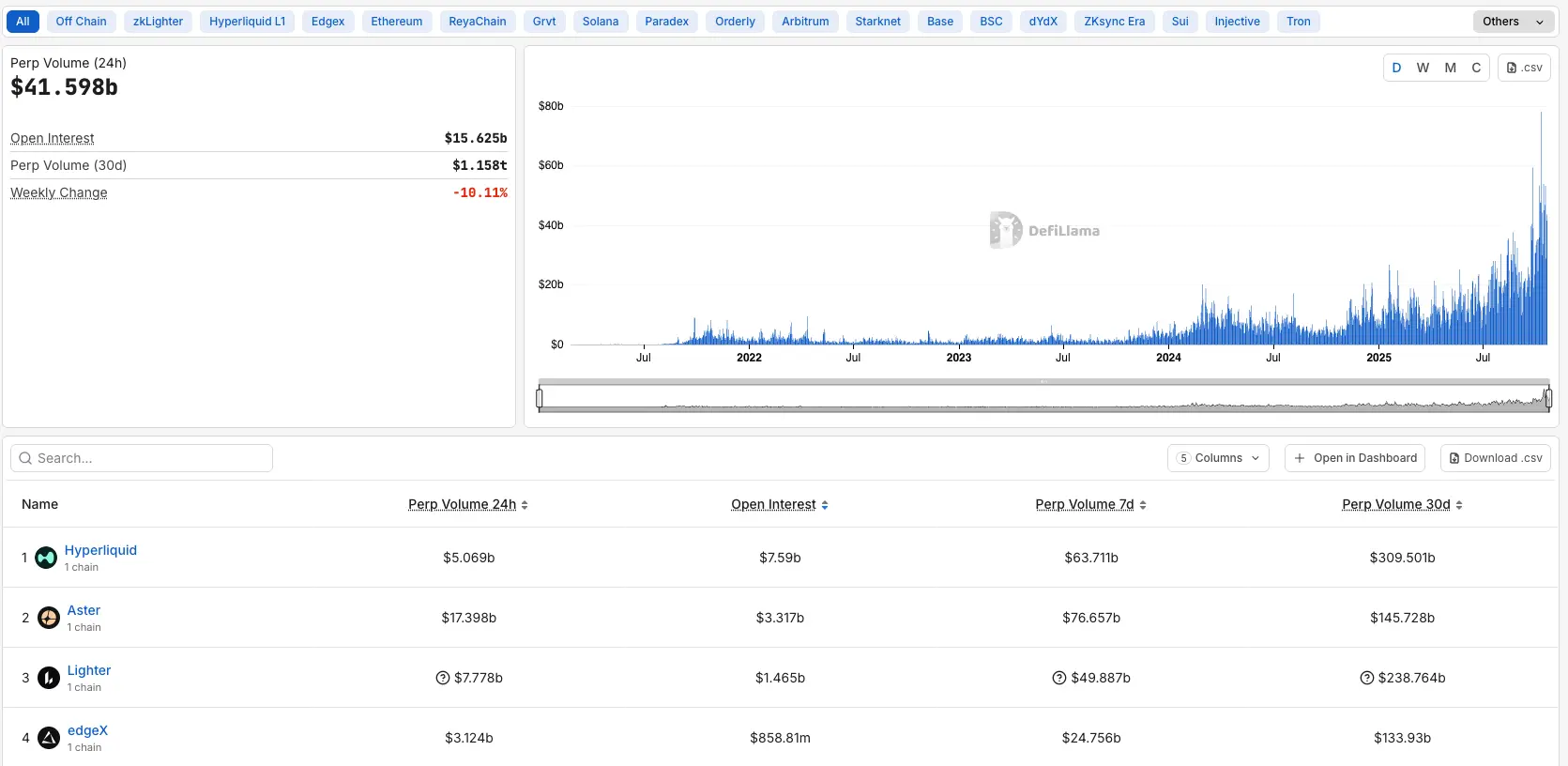

ข้อมูล DeFillama วันนี้ (2025.10.20):

ปริมาณ 24 ชั่วโมงของ Perp DEX ทั้งหมดอยู่ที่ 41B, OI อยู่ที่ 15B โดย Hyperliquid ยังคงเป็นผู้นำตลาด ครอง OI ประมาณ 50%, Aster ครองประมาณ 20%, Lighter ครองประมาณ 10%, edgeX ครองประมาณ 5.5% หมายความว่า F4 ครองส่วนแบ่งรวมประมาณ 85%

Perp DEX อีกหลายร้อยแห่งแบ่งกัน 15% ที่เหลือ ผลกระทบของผู้นำตลาดเห็นได้ชัดเจน

*ที่นี่ใช้การจัดอันดับตาม OI ไม่ใช่ Volume เพื่อขจัดการ wash trading และแสดงศักยภาพที่แท้จริงมากขึ้น

นอกจากนี้ยังสามารถวิเคราะห์ข้อมูล OI/Volume ratio ได้อีกด้วย ค่ายิ่งสูงหมายถึง“ปริมาณเทรดและผู้ใช้จริงมากขึ้น ค่ายิ่งต่ำหมายถึงการ wash trading มากขึ้น”

Hyperliquid ประมาณ 1.5, Aster และ Lighter ประมาณ 0.19, edgeX ประมาณ 0.27

Hyperliquid มี OI/Volume ratio สูงสุด แสดงว่าผู้ใช้มีโฮลดิ้งส์สูงหรือถือฟิวเจอร์สระยะยาวมาก; Aster และ Lighter มีปริมาณเทรดสูงแต่ OI ต่ำ แสดงว่าการเทรดระยะสั้นและการเปลี่ยนตำแหน่งสูง (มีการ wash trading มาก); edgeX อยู่ระดับกลาง OI/Volume ประมาณ 0.27 ความลึกและความเคลื่อนไหวของตลาดค่อนข้างสมดุล แต่ยังห่างจาก Hyperliquid มาก

edgeX Points แผนการสะสมแต้มเทรด

คล้ายกับ Lighter, edgeX Points เป็นแต้มหลายมิติ “ข้อตกลงรายสัปดาห์ (ปัจจุบันสัปดาห์ที่ 20) แบ่งตามการมีส่วนร่วม” เพื่อรางวัลแก่การเทรดจริงและการมีส่วนร่วมในระบบนิเวศ

Open Season ปัจจุบันมีน้ำหนัก: ปริมาณเทรด 60%, การเชิญ/ทูต/กิจกรรม 20%, กองทุนและ TVL 10%, การล้างบัญชี 5%, โฮลดิ้งส์ (OI) 5%; ข้อตกลงทุกวันพุธ 00:00 UTC แจกจ่ายวันพฤหัสบดี 08:00 UTC

การคำนวณแต้มรวมถึงปริมาณเทรด, ปริมาณเทรดของผู้ใช้ที่ถูกแนะนำ, โฮลดิ้งส์ (OI), ความถี่ในการใช้ฟีเจอร์ น้ำหนักสามารถปรับเปลี่ยนได้ มีการแบ่งรางวัลเป็น 5 ระดับตามปริมาณเทรดทั่วโลกต่อสัปดาห์ ปกติ 150,000 หรือ 200,000 แต้ม; ตัวเลขจริงอาจเปลี่ยนแปลง เช่น Open Season สัปดาห์ที่ 20 แจกจ่าย 300,000 แต้มให้กับ 13,668 ที่อยู่ การเชิญและเงินคืน ทุกครั้งที่ผู้ใช้ที่ถูกแนะนำได้รับ 5 แต้ม ผู้แนะนำได้ 1 แต้ม (20%) กฎต่อต้านการ wash trading/self-trade ไม่คิดแต้ม; แพลตฟอร์มสามารถตัดธุรกรรมผิดปกติได้ ทางการระบุชัดเจน: วิธีคำนวณและน้ำหนักอาจปรับเปลี่ยน

กลยุทธ์คุ้มค่าในการเก็บแต้ม (เพื่อการศึกษา ไม่ใช่คำแนะนำการลงทุน รับผิดชอบความเสี่ยงเอง)

รวมปริมาณเทรดไว้ที่บัญชีหลักเดียว เพิ่ม VIP เพื่อลดค่าธรรมเนียมเทรด ลดต้นทุน เน้นการตั้งคำสั่งเพื่อรับค่าธรรมเนียมต่ำสุด

คล้ายกับ Lighter, หลีกเลี่ยง self-trade และการเทรดระยะสั้นมาก; ควรถือฟิวเจอร์สนานขึ้นเพื่อได้ “ปริมาณเทรด+OI”

เข้าร่วม eStrategy/eLP กองทุนเพื่อรับส่วนแบ่ง “Vault/TVL 10%” และผลตอบแทนที่ได้ที่อาจเกิดขึ้น เข้าร่วมกิจกรรมทางการและแผนทูตเพื่อรับน้ำหนัก “20%” ควบคุมความเสี่ยงจากเลเวอเรจและการล้างบัญชี แต้มล้างบัญชีมีแค่ 5% กิจกรรม NFT สามารถเข้าร่วมตามความเหมาะสม ถือเป็นนวัตกรรมด้านการดำเนินงาน ชื่นชอบ ทางการระบุชัดเจนว่า NFT ผูกกับแอร์ดรอปโทเคนการกำกับดูแล มีแค่ 299 ชิ้น edgeX ยังสามารถอ้างอิงแอร์ดรอป meme ของ Hyperliquid แจกแคนดี้ให้สายเก็บแต้มก่อน

ข้อมูลปัจจุบัน แจกจ่ายรวม 3,471,363 Points (Open Season สัปดาห์ที่ 1–20)

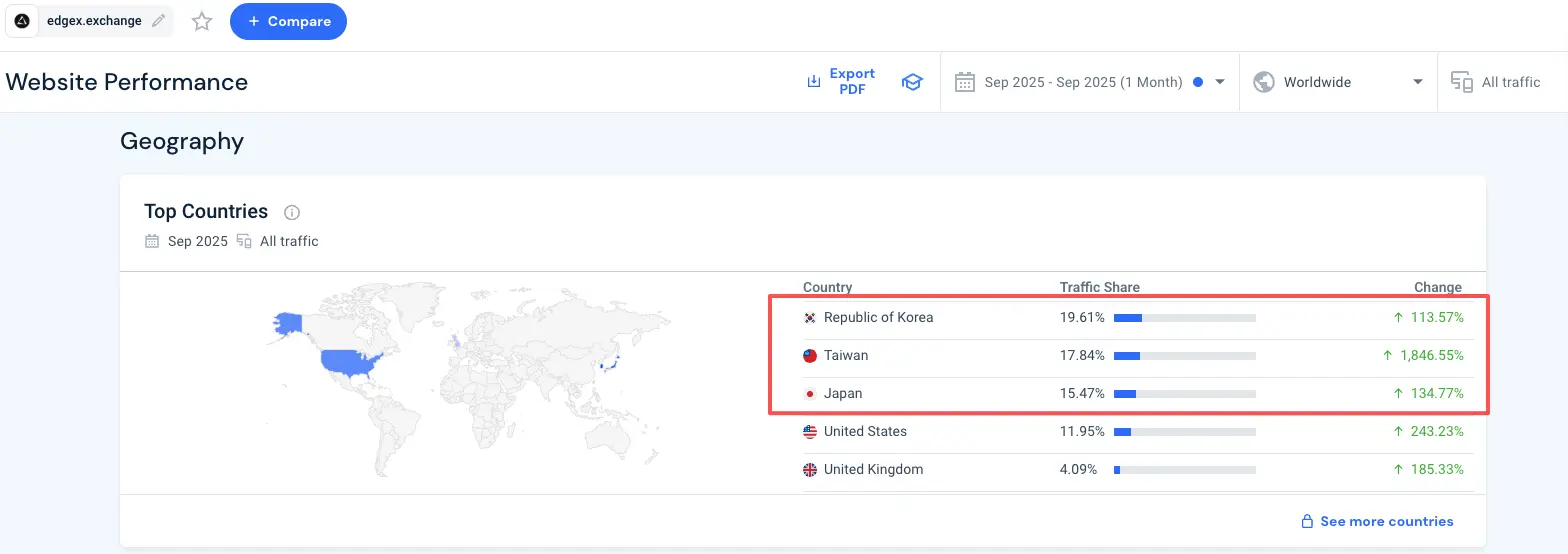

edgeX การกระจายผู้ใช้

การกระจายผู้ใช้ edgeX กับ Aster มีความซ้ำซ้อนสูง โดยเน้นที่เอเชีย โดยเฉพาะจีนและญี่ปุ่น/เกาหลี แม้ว่า Aster จะเน้นตลาดยุโรปและอเมริกาแล้ว แต่กลุ่มหลักยังอยู่ที่ CN

ตามข้อมูลการเข้าชมเว็บไซต์ (จาก similarweb) ญี่ปุ่น เกาหลี และไต้หวันรวมกันครึ่งหนึ่ง ยังมีผู้ใช้จีนแผ่นดินใหญ่ที่ใช้ VPN กระจายอยู่ทั่วโลก จากสถานการณ์ชุมชน CN ก็มีสัดส่วนไม่น้อย

เปรียบเทียบกองทุน

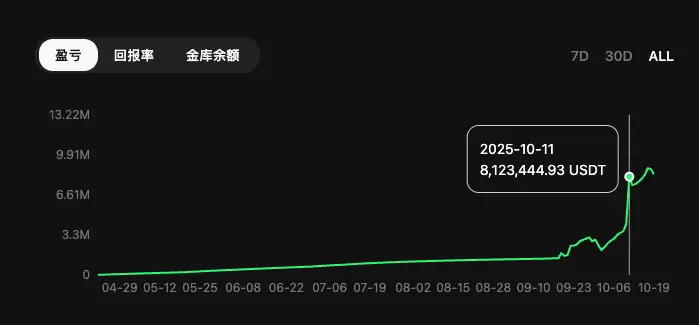

เหมือนกับ HLP และ LLP, eLP (edgeX Liquidity Pool) คือกองทุนสภาพคล่องของ edgeX (ดูภาพด้านล่าง)

รายได้ของ edgeX eLP ปัจจุบันมาจากกำไรการทำตลาดแบบ passive, ค่าธรรมเนียมการล้างบัญชี และส่วนหนึ่งของค่าธรรมเนียมเทรดของแพลตฟอร์ม ในเฟสถัดไป eStrategy จะนำกองทุนที่ปรับแต่งได้โดยเทรดเดอร์หรือสถาบันเข้ามา จุดนี้ eLP ยังตามหลัง HLP และ LLP อยู่หนึ่งขั้น HLP และ LLP ตอนนี้มีทั้ง “โปรโตคอลกองทุน” + “กองทุนผู้ใช้”

เปรียบเทียบ 3 เจ้า, Aster’s ALP ไม่พูดถึง ALP ใช้แค่ในโหมด Simple 1001x มีแค่หลักสิบล้าน

อันดับ TVL กองทุน (2025.10.20): HLP $628m อันดับหนึ่ง, LLP $503m อันดับสอง (กองทุนผู้ใช้ไม่คิด), eLP $147m อันดับสาม อีกเรื่อง ในช่วงลดราคาครั้งใหญ่ 1011, eLP และ HLP ทำกำไรได้, LLP ขาดทุน (สุดท้ายจ่ายแค่แต้ม)

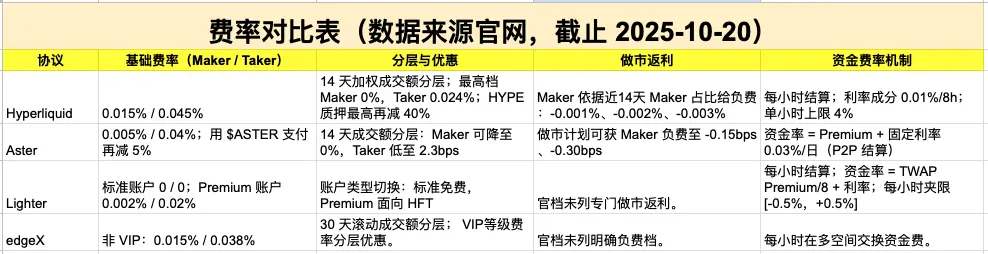

เปรียบเทียบค่าธรรมเนียมเทรด

ค่าธรรมเนียมเทรดของ Perp DEX F4 มีจุดเด่นต่างกัน นักลงทุนรายย่อยและเทรดต่ำเลือก Lighter มาตรฐาน (0 ค่าธรรมเนียมเทรด), เทรดความถี่สูงเลือก Lighter Premium, ทำตลาดแบบ passive และเทรดปริมาณมากเลือก Aster หรือ Hyperliquid, ผู้ที่ไวต่อการเปลี่ยนแปลง funding fee เลือก Aster และ Lighter edgeX โครงสร้างค่าธรรมเนียมเทรดดูเหมือนจะไม่โดดเด่น

สุดท้ายคุยเรื่องตลาด Perp DEX

FTX ใช้เงินลูกค้าผิดวัตถุประสงค์, หลาย CEX เล่นพนันกับผู้ใช้, ผู้นำในคัดลอกการเทรด, แก้ไขกราฟราคา, ควบคุมตลาด ฯลฯ เหตุการณ์เหล่านี้กัดกร่อนความเชื่อมั่นของผู้ใช้ต่อ CEX ความเชื่อมั่นต่อ CEX ลดลงต่ำสุด ฝั่งผู้ให้บริการ CEX ก็ถูกกดดันจากการปฏิบัติตามกฎระเบียบทั่วโลก จึงต้องปรับตัวไปสู่ DEX/โครงสร้าง self-custody ฝั่งผู้ใช้ก็เพราะปัญหาความเชื่อมั่น, KYC, และประสบการณ์ DEX ที่ดีขึ้นเรื่อย ๆ จึงค่อย ๆ เปลี่ยนไปใช้ DEX

แก่นของ Perp DEX คือการนำการจับคู่, การล้างบัญชี, ควบคุมความเสี่ยง และการดูแลทรัพย์สินของ CEX มาไว้ในชั้นฟิวเจอร์ส/การพิสูจน์ที่ตรวจสอบได้ พร้อมทั้งพยายามลด latency และเพิ่มความลึก จุดต่างหลักคือ “ความสามารถในการตรวจสอบได้” การจัดลำดับคำสั่ง, การจับคู่, การล้างบัญชีของ CEX เป็นกล่องดำและต้องอาศัยความเชื่อใจ; Perp DEX ใช้การดำเนินการ on-chain และการพิสูจน์ความถูกต้อง ให้ “ราคา+เวลา” และ “ล้างบัญชีตามกฎ” พิสูจน์ตัวเองด้วยการเข้ารหัสข้อมูลและชั้นสัญญา ลดโอกาสการโกง การดูแลทรัพย์สิน CEX มีความเสี่ยงระเบิดและถูกแช่แข็ง; Perp DEX ใช้ฟิวเจอร์สดูแลทรัพย์สิน ร่วมกับ priority tx/ช่องทางหนี ผู้ใช้ถือกุญแจส่วนตัว สามารถออกจากระบบได้อย่างปลอดภัยเมื่อเกิดปัญหา

เชื่อคณิตศาสตร์มากกว่าคน, in math we trust, code is law คือแก่นของบล็อกเชน, Perp DEX คือความโปร่งใสและแก้ไขไม่ได้ของบล็อกเชน

ตอนนี้ตลาด Perp DEX เริ่มลงตัว Hyperliquid นำด้วยความลึกและประสิทธิภาพ; Aster, Lighter แข่งด้วยรางวัลและนวัตกรรมฟีเจอร์; edgeX แตกต่างโดยเน้นมือถือและการดำเนินงานที่มั่นคง สร้างชื่อเสียงในเอเชีย ปัจจัยชี้ขาดคือความง่ายในการใช้งาน, การประสานทรัพยากรในระบบนิเวศ และความยั่งยืนของรางวัล; ผู้ใช้ระยะสั้นสามารถเทรดข้ามแพลตฟอร์มเพื่อเก็บแต้ม ระยะยาวต้องดูการสร้างรายได้และความเหนียวแน่นของชุมชน

ด้านการเล่าเรื่องและการแข่งขัน ความฮอตของ Perp DEX กำลังลดลง หน้าต่างแอร์ดรอปใหญ่มีแนวโน้มปิดในปี 2025 รอบถัดไปคือตลาดทำนาย (เช่น YZi Labs กำลังดูโปรเจกต์ Prediction Market, Hyperliquid HIP-4 ก็เกี่ยวกับตลาดทำนาย) สายเก็บแต้มหลายคนเริ่มเปรียบเทียบ Perp DEX กับ L2 ในอดีต รอบใหญ่ใน OP/ARB/STRK, หลัง ๆ กลยุทธ์ pullback มากขึ้น; HYPE, ASTER, LIGHTER, edgeX ผลตอบแทนอาจลดลง ผู้เล่นใหม่อาจโดน “สวนกลับ” Perp DEX เก็บแต้มอาจกลายเป็น “L2 ถัดไป” ก็เป็นไปได้ ขณะที่ Hyperliquid กับ Aster แข่งกันดุเดือด, F4 เป็นผู้นำตลาด อีกด้านปีหน้าหลักอาจเปลี่ยนไปตลาดทำนาย ปีนี้ก่อนสิ้นปี ใครที่ยัง TGE ไม่ได้, ข้อมูลเริ่มต้นไม่ดี, ระบบนิเวศซ้ำซ้อน ไม่มีแบ็คอัพ ต้องระวัง ส่วนผู้ใช้ฟิวเจอร์สจริงที่ย้ายบางตำแหน่งจาก CEX ไป Perp DEX ที่ยังไม่ TGE สามารถเก็บแต้มได้หลายทาง

เจ้าของ CEX ที่กำลังพัฒนา Perp DEX ต้องเร่งมือ ขณะที่ยังมี buff แอร์ดรอป, meme แอร์ดรอป, NFT mint, แข่งเทรดแต้ม… รีบกิน buff… ความเร็วสำคัญกว่าความสมบูรณ์

สายเก็บแต้มจากการเทรด Perp DEX รีบเทรดกับผู้นำ, โปรเจกต์ดี ๆ รีบเข้า ยิ่งช้าจะยิ่งยาก รีบเก็บแล้วเปลี่ยนไปตลาดทำนาย… เลือกให้ถูกสำคัญกว่าขยัน

สุดท้าย ขอให้ทุกคนร่ำรวย

(ข้างต้นเป็นความเห็นส่วนตัว ไม่ใช่คำแนะนำการลงทุน หากมีข้อผิดพลาดยินดีรับฟัง)