Author: Prathik Desai

Translated and Edited by: BitpushNews

More than a year ago, becoming a cryptocurrency reserve company (DAT) seemed like an easy decision for many firms seeking to boost their stock prices.

Some Microsoft shareholders convened to urge the board to evaluate the benefits of including Bitcoin on their balance sheets. They even mentioned Strategy, the largest publicly listed Bitcoin DAT.

At that time, a financial flywheel was in place, attracting everyone to follow.

Buy large amounts of Bitcoin, Ether, Solana (SOL). Watch the stock price trade above the value of these assets. Issue more shares at a premium. Use the proceeds to buy more cryptocurrencies. Repeat. This financial flywheel supporting publicly traded stocks seemed almost perfect, enough to tempt investors. They paid over two dollars just to gain indirect exposure to Bitcoin worth only one dollar. It was a crazy era.

But time tests the best strategies and flywheels.

Today, with over 45% of the total crypto market cap evaporated in the past four months, most of these packaged companies’ market-to-net-asset-value ratios have fallen below 1. This indicates that the market values these DAT companies below the worth of their crypto reserves. This has changed how the financial flywheel operates.

Because a DAT is not just a packaging of assets. In most cases, it’s a company with operating expenses, financing costs, legal, and operational fees. During the mNAV premium era, DATs raised funds by issuing more shares or taking on more debt to buy cryptocurrencies and cover operational costs. In the mNAV discount era, this flywheel collapses.

In today’s analysis, I will show what a persistent mNAV discount means for DATs and whether they can survive a crypto bear market.

Between 2024 and 2025, over 30 companies are vying to transform into DATs. They are building reserves around Bitcoin, Ether, SOL, and even meme coins.

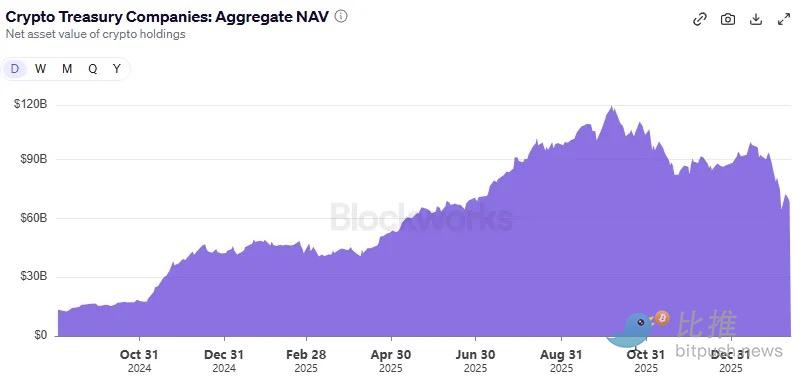

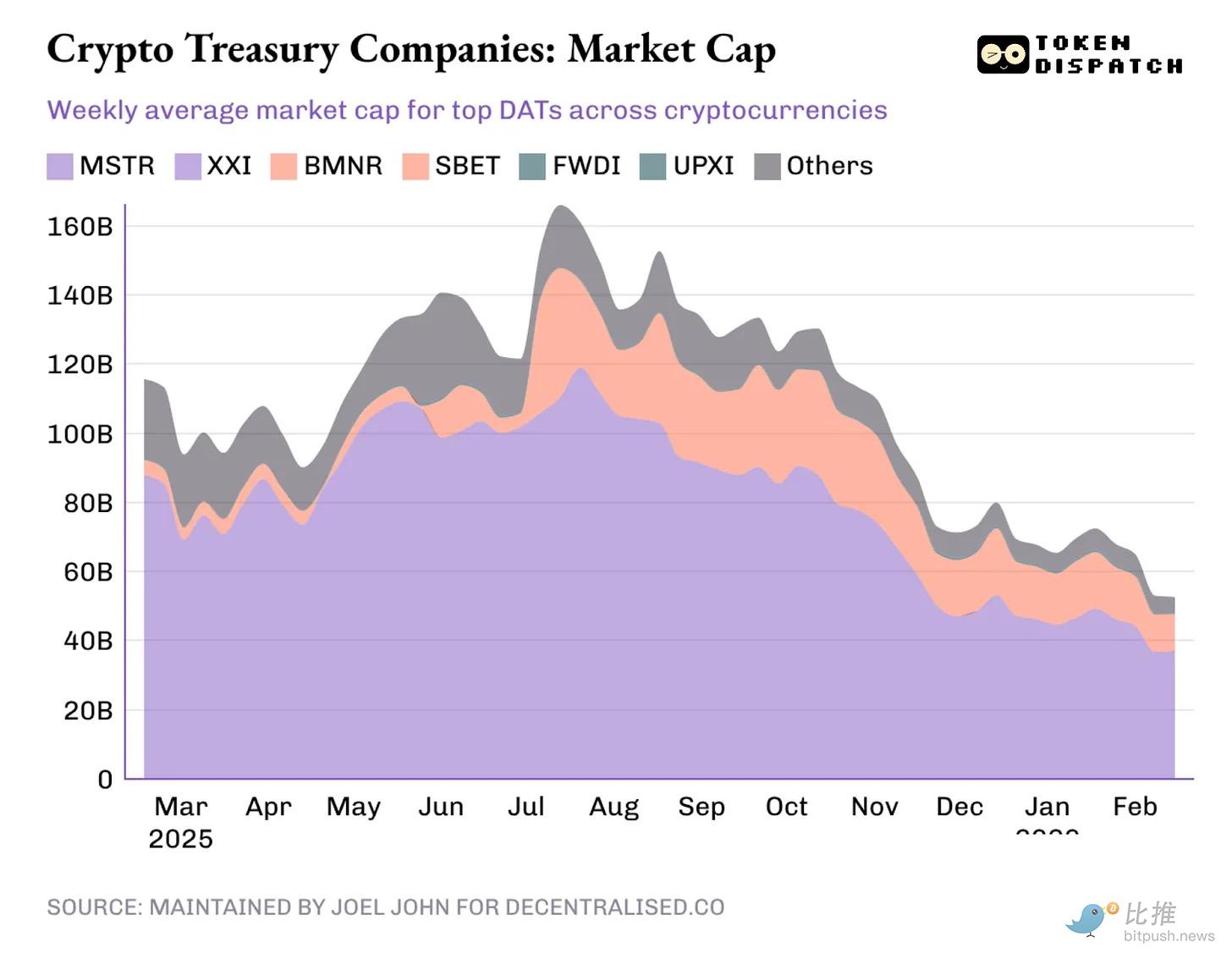

At the peak on October 7, 2025, the crypto held by DATs was valued at $118 billion, with these companies’ total market cap exceeding $160 billion. Today, the crypto holdings are worth $68 billion, and their discounted total market cap is just over $50 billion.

Their fates all hinge on one thing: their ability to package assets and weave stories that justify a valuation higher than the assets’ worth. This difference becomes the premium.

The premium itself becomes a product. If the stock trades at 1.5 times mNAV, a DAT can sell stock worth $1, then buy crypto exposure worth $1.50, and describe this transaction as “value-added.” Investors are willing to pay a premium because they believe the DAT can continue selling shares at a premium and use the proceeds to accumulate more crypto, thereby increasing the per-share crypto asset value over time.

The problem is, premiums don’t last forever. Once the market stops paying extra for this packaging, the “sell stock, buy coins” flywheel stalls.

When stocks no longer trade at 1.5 times asset value, the amount of crypto bought with each new share issuance decreases. The premium turns into a discount.

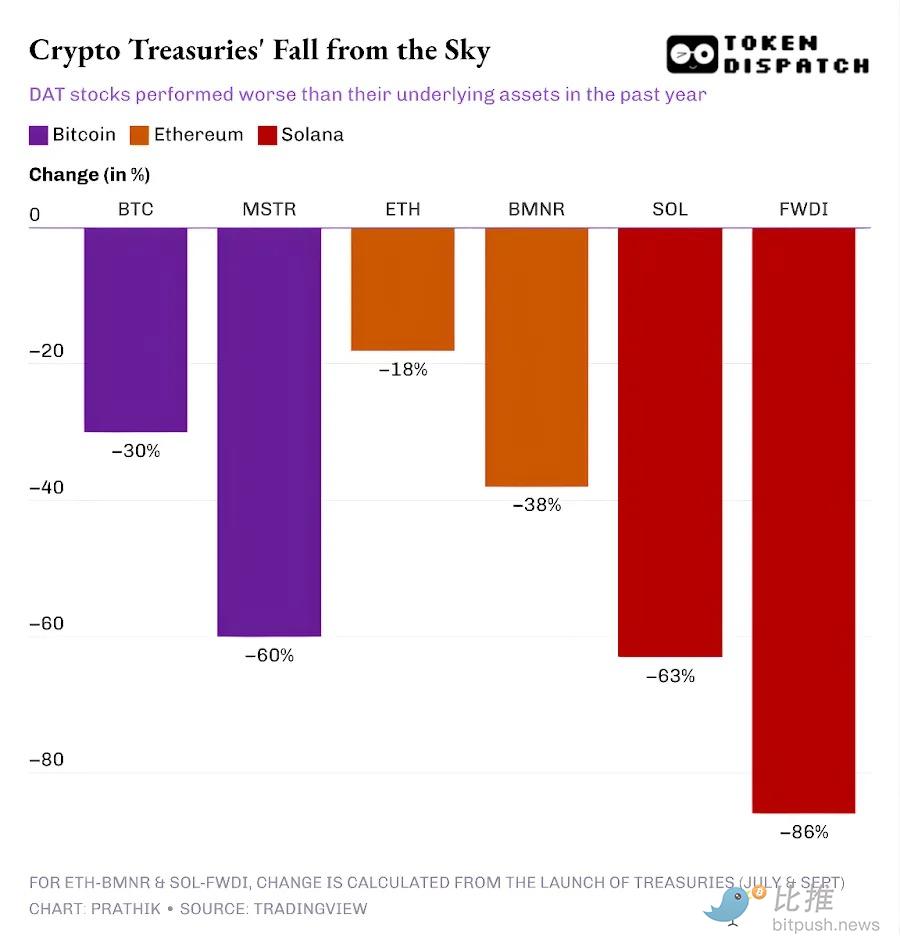

Over the past year, leading Bitcoin, Ether, and SOL DATs’ stock prices have fallen more than the cryptocurrencies themselves.

Once the premium relative to the underlying assets disappears, investors will naturally ask: why can’t they buy crypto directly elsewhere, such as on decentralized or centralized exchanges, or through exchange-traded funds, at a cheaper price?

Bloomberg’s Matt Levin posed an important question: if the trading price of a DAT doesn’t even reach its net asset value, let alone a premium, why don’t investors push the company to liquidate its crypto reserves or buy back stock?

Many DATs, including the industry leader Strategy, try to convince investors that they will hold crypto through the bear cycle, waiting for the premium era to return. But I see a more critical issue. If a DAT cannot raise additional funds in the foreseeable long term, where will it get the money to operate? These DATs have bills and wages to pay.

Strategy is an exception, for two reasons.

-

According to reports, it holds $2.25 billion in reserves, enough to cover dividends and interest obligations for about 2.5 years. This is significant because Strategy no longer relies solely on zero-coupon convertible bonds for fundraising. It has also issued preferred instruments that require paying substantial dividends.

-

It also has an operational business, no matter how small, that can generate recurring income. In Q4 2025, Strategy reported total revenue of $123 million, with a gross profit of $81 million. Although Strategy’s net profit may fluctuate significantly due to quarterly changes in crypto asset valuations, its business intelligence division is the company’s only tangible cash flow source.

But this still doesn’t make Strategy’s strategy invulnerable. The market can still punish its stock—as it has over the past year—and weaken Strategy’s ability to raise funds at low cost.

While Strategy might survive the crypto bear market, emerging DATs lacking sufficient reserves or operational businesses to cover unavoidable expenses will feel the pressure.

This difference is even more apparent in Ether-based DATs.

The largest Ether-based DAT—Bitmine Immersion—has a marginalized operational business supporting its Ether reserves. As of the quarter ending November 30, 2025, BMNR reported total revenue of $2.293 million, including consulting, leasing, and staking income.

Bitmine’s balance sheet shows the company holds digital assets valued at $10.56 billion and $887.7 million in cash equivalents. BMNR’s operations resulted in a net negative cash flow of $228 million. All cash needs are met through issuing new shares.

Last year, since BMNR’s stock traded at a premium to mNAV most of the time, raising funds was relatively easy. But over the past six months, the mNAV has dropped from 1.5 to about 1.

So what happens when the stock no longer trades at a premium? Issuing more shares at a discount could lower the per-share Ether price, making it less attractive to investors than buying Ether directly from the market.

This explains why BitMine announced last month it would invest $200 million to acquire shares of Beast Industries, a private company owned by YouTuber MrBeast. The company said it would “explore ways to collaborate on DeFi projects.”

Ether and SOL DATs might also argue that staking income—something Bitcoin DATs can’t boast—can help them operate during market crashes. But this still doesn’t solve the issue of meeting cash flow obligations.

Even with staking rewards (accumulated in Ether or SOL), as long as these rewards aren’t exchanged for fiat currency, DATs can’t use them to pay wages, audit fees, listing costs, or interest. Companies must either have sufficient fiat income or sell or re-mortgage reserves to meet cash needs.

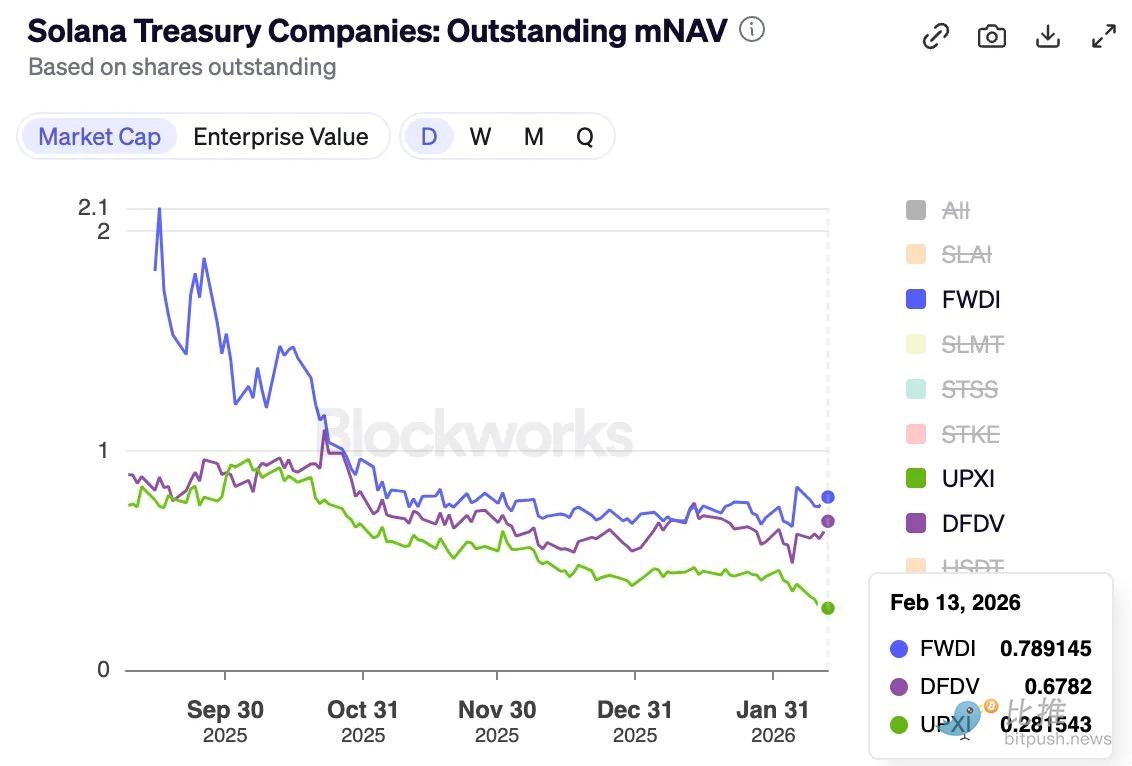

This is especially evident in the largest SOL holder—Forward Industries.

FWDI reported a net loss of $586 million in Q4 2025, despite earning $17.381 million in staking and related income.

Management explicitly stated that the company’s “cash balance and working capital are sufficient to meet our liquidity needs at least until February 2027.”

FWDI also disclosed an active capital-raising strategy, including issuing stock at market price, buybacks, and a tokenization experiment. However, if the mNAV premium persists long-term, all these efforts may fail to manage the packaging’s valuation.

Future Outlook

Last year’s DAT craze centered on the speed of asset accumulation and the ability to raise funds through issuing shares at a premium. As long as the packaging trades at a premium, DATs can continue converting expensive equity into more crypto per share, calling it “beta.” Investors also pretend the only risk is the asset price itself.

But premiums won’t last forever. Crypto cycles can turn them into discounts. I first raised this issue shortly after the October 10, 2022, liquidation event when I observed the premium decline.

However, this bear market will push DATs to evaluate: once the packaging no longer trades at a premium, should they still exist?

One way to address this dilemma is for companies to improve operational efficiency, using profitable businesses or surplus reserves to supplement DAT strategies. Because when the story no longer attracts investors during a bear market, a conventional company story will determine survival.

If you’ve read the article “Strategy & Marathon: Faith and Power,” you’ll recall why Strategy has remained resilient across multiple crypto cycles. However, a new wave of companies like BitMine, Forward Industries, SharpLink, and Upexi cannot rely on the same strength.

Their current attempts at staking income and weak operational businesses may collapse under market pressure unless they consider other options to cover real-world obligations.

We saw this with ETHZilla, an Ether reserve company that last month sold about $115 million worth of Ether and bought two jet engines. Subsequently, the DAT leased the engines to a major airline and hired Aero Engine Solutions for monthly management fees.

Looking ahead, market participants will evaluate not only digital asset accumulation strategies but also their ability to survive. In the ongoing DAT cycle, only those that can effectively manage dilution, debt, fixed obligations, and trading liquidity will weather the downturn.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.

Related Articles

Bitcoin ETF Sees Daily Outflow of $16.03M While Ethereum and Solana ETFs Record Gains on April 27

Gate News message, according to the April 27 update, Bitcoin ETF recorded a daily net outflow of 209 BTC ($16.03 million), while maintaining a weekly net inflow of 9,987 BTC ($767.27 million). Ethereum ETF showed a daily net inflow of 24 ETH ($56,000) and a weekly net inflow of 41,013 ETH ($93.35 mi

GateNews59m ago

Coinshares: $1.2B Crypto Inflow, Bitcoin Leads Fund Flows

Cryptocurrency investment products received $1.2 billion in inflows last week, marking the fourth consecutive positive week, according to a Coinshares report. Bitcoin surged above $79,000 before Asian market opening, though the move was short-lived, with BTC subsequently dropping to around $77,600.

CryptoFrontier2h ago

Ethereum Outperforms S&P 500 by 1,696 Basis Points Since U.S.-Iran Conflict, Says Tom Lee

Gate News message, April 27 — Tom Lee, chairman of Bitmine, stated that Ethereum has outperformed the S&P 500 index (U.S. benchmark equity index) by 1,696 basis points since the U.S.-Iran conflict, making it the best-performing single asset globally aside from crude oil. According to Lee, ETH has de

GateNews2h ago

Bitmine increased its holdings by more than 100,000 ETH last week, and its total holdings exceeded 5 million ETH units/coins.

Bitmine’s total ETH holdings have surpassed 5 million coins, accounting for 4.21% of the supply. Last week, it increased its holdings by more than 100,000 coins. This article analyzes the cadence of institutional holdings, the impact of on-chain concentration, and market outlook scenarios.

GateInstantTrends2h ago

ETH Liquidation Data: $1.254B in Short Liquidations at $2,424, $641M in Long Liquidations at $2,212

Gate News message, April 27 — According to Coinglass data, if Ethereum (ETH) breaks above $2,424, cumulative short liquidations on major centralized exchanges would reach $1.254 billion.

Conversely, if ETH falls below $2,212, cumulative long liquidations on major CEXs would reach $641

GateNews3h ago

Galaxy Digital OTC Address Deposits 15,000 ETH to Exchange, Worth ~$34.74M

Gate News message, April 27 — Galaxy Digital's OTC-linked address deposited 15,000 ETH, valued at approximately $34.74 million, to an exchange today, according to on-chain analyst Ai 姨.

Tracing the funds backward, the ETH batch originated from a 38,000 ETH withdrawal from Aave one week ago.

GateNews3h ago